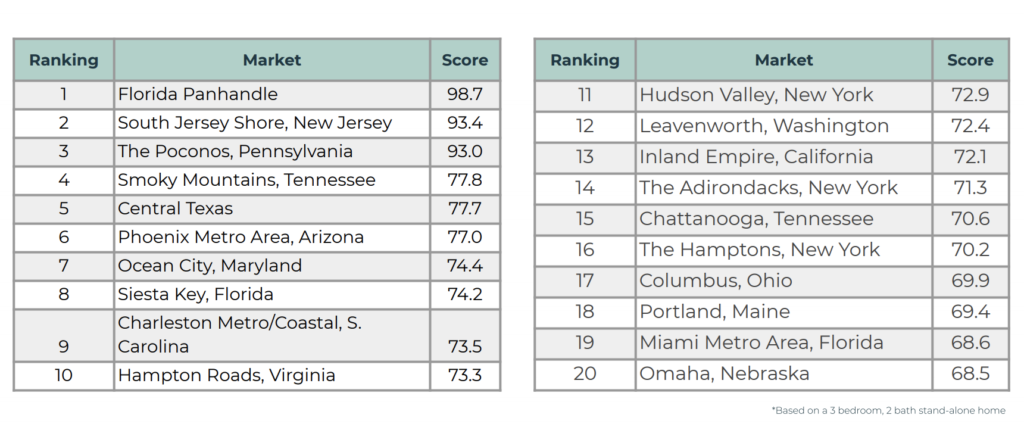

from Inman Property Portfolio, 7-21-2020 As the pandemic lingers into the summer months, real estate investors are carefully examining their portfolios and identifying growth opportunities. While single-family or multifamily rentals may not be as lucrative as rents decline, rental management site Rented Inc.’s said investors might find their golden egg in Florida’s vacation rental market. According to Rented’s latest market report with Weiss Analytics, published on 7-20-2020, vacation properties along the Florida Panhandle offer the best return on investment, due to a relatively low cost of ownership and acquisition cost matched with healthy short-term revenue potential, annual home value appreciation and future asset value gains.  The Florida Panhandle, which includes Tallahassee and Pensacola, received a score of 98.7 out of 100, which reflects the robust return on investment for a three-bedroom, two-bathroom single-family home. The South Jersey Shore (93.4), the Pennsylvania Poconos (93.0), the Smoky Mountains (77.8), and Central Texas (77.7) round out the top five best places to invest. “Our findings uncover the most lucrative locations to buy real estate where the cost of ownership is outweighed by the returns vacation rentals provide,” Rented, Inc. CEO Andrew McConnell explained in a prepared statement. “Hospitality is still front and center, but it’s become clear that there is more to vacation rental investment management than finding a property and someone to keep things clean.” To stay competitive, the report said investors must invest in smart home technology to accommodate renters who are working during extended stays. Furthermore, investors must be able to offer a seamless, totally digital experience, as travelers aim to reduce in-person contact during the pandemic, it added. “Our bustling global economy came to a screeching halt with the travel industry at the center of near collapse,” the report read. “What we’re seeing now is two years of innovation happening in a quarter! Remote work, video conferencing, longer stays, and no-contact check-ins, once optional, are now essential.”

0 Comments

As we move through the next few months, take the time to do several of the following to “refresh” your home. It will also add value if you decide to sell in 2021!

1. ‘Closing an old account will help my credit’ This might be one of the most common misconceptions around how unused accounts, like credit cards, can impact creditworthiness. One of the main factors that lenders look at when reviewing your clients’ credit history is how long accounts have been open. They typically average all current and past accounts to get an average length of time. The longer your credit history, the better. By closing an old account, you are effectively reducing the impact that individual account may have on your overall credit history. Instead of closing the account, keep it open. 2. All debt is treated equally Since all debt carries a monetary value, it might make sense that all debt is the same. However, this is not the case. Lenders look at the specific type of debt to better understand the risk associated with it. Short-term accounts, like credit or charge cards, are considered more risky if the account has a high amount of revolving debt. This is due, in part, to the requirement that credit cards be paid off monthly. In contrast, a 30-year mortgage is understood to be a long-term debt and is treated as such. Therefore, just because your clients have a car loan with a high balance remaining, does not mean that it will hurt their credit as much as a credit card that is maxed out. 3. ‘Credit repair companies can help improve my credit’ The old adage of “if something is too good to be true, it probably is” couldn’t be more accurate in this example. Buyers have become increasingly interested in getting help establishing or repairing their credit. Companies such as Credit Karma, Credit Sesame, and even the major three credit reporting companies such as Equifax, Experian and TransUnion offer ways to improve or “boost” credit. However, these companies can only assist you with creating a plan to pay down or consolidate debt. They cannot magically make or reduce the amount of debt a person has — this can only be done by paying off an account. Instead of paying a company to put this plan together, homebuyers can create a spreadsheet with their recurring expenses along with their monthly income to visualize and plan for what debts can be paid down over a period of time. 4. ‘Paying off a collection or debt removes it from my credit report’ Undeniably false. In fact, a derogatory mark like a collection or missed payment can stay on your credit report for up to seven years. While paying this off will stop future attempts by the collection agency or banking institution to collect on the debt, there is no way to remove a derogatory mark from your credit report unless it was reported incorrectly due to fraud or identity theft. 5. ‘My relationship status or divorce is reflected on my credit report’ Information like income, employment and relationship status are not reported to credit bureaus. Questions regarding this information will likely be asked during the credit application process in conjunction with the review of your credit score.

For baby boomers, the question of when—and where—they'll retire is a perennial topic of discussion. But with the novel coronavirus sweeping the globe, it has become an especially pressing question these days. Many are feeling the pressure to ramp up their decision-making and act fast—between concerns over COVID-19 contagion, rampant layoffs, and new rounds of self-reckoning where they ponder "Why wait to realize my dreams?" Many believe that the time is now to make real estate decisions they've been putting off. 'COVID-19 convinced me to move to my retirement home early' David, 66, who lives in Boston, thought he’d stay a New Englander for a few more years. But the COVID-19 pandemic galvanized his long-simmering plans to head south.

“I grew up in Georgia and miss some aspects of Southern life, including the weather,” he explains. "That becomes a bigger deal every year. But I wanted to keep earning as much as I could until age 70, the way you’re supposed to if you want the biggest Social Security income.” However, since he works in fundraising for an arts organization, he’s seen his work hours dramatically reduced since COVID-19 came to town. “Our organization came to almost a full stop, and, while still employed, I took a significant salary cut," he says. "And the fact that the arts will be among the last areas to reopen in hard-hit states makes me think my work life is over.” David chooses to look at this as a glass half-full. “It's a sign to move on to the next phase of life,” he says. "I've been talking about buying a little, cheap, beach-bum place in Florida for years. Now, I'm ready. This virus has brought me face to face with my mortality. The time to realize my dreams is now. There are no guarantees." He is actively searching online for a cottage or condo near the water in the vicinity of Tallahassee, FL. Working with a local real estate agent, he’s doing virtual walk-throughs on FaceTime. While he's not sure if he'll actually buy a house sight unseen, he's excited to be laying the groundwork for the next phase of his life. "The idea of having a laid-back life, listening to the surf, going fishing in Florida, that will be heaven! For me, this tragedy has a silver lining.” |

RSS Feed

RSS Feed